Last Friday, May 10th, Concord-Carlisle High School hosted “The Game of Life Reality Fair” for seniors during Flex Block. Organized by Mrs. Melea Ray, the purpose of the reality fair was to prepare seniors–who will be graduating very soon–for real-world financial situations and equip them with the crucial tools of budgeting and money management.

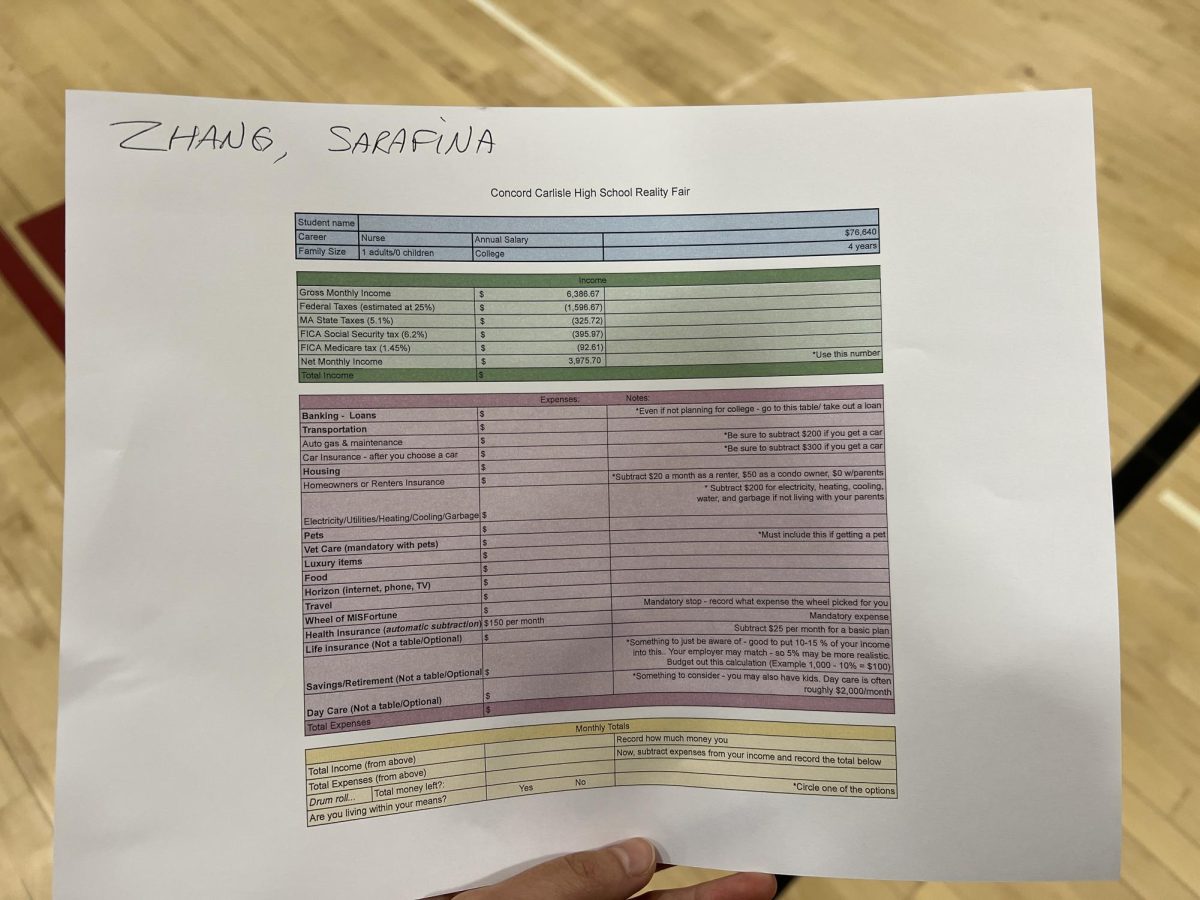

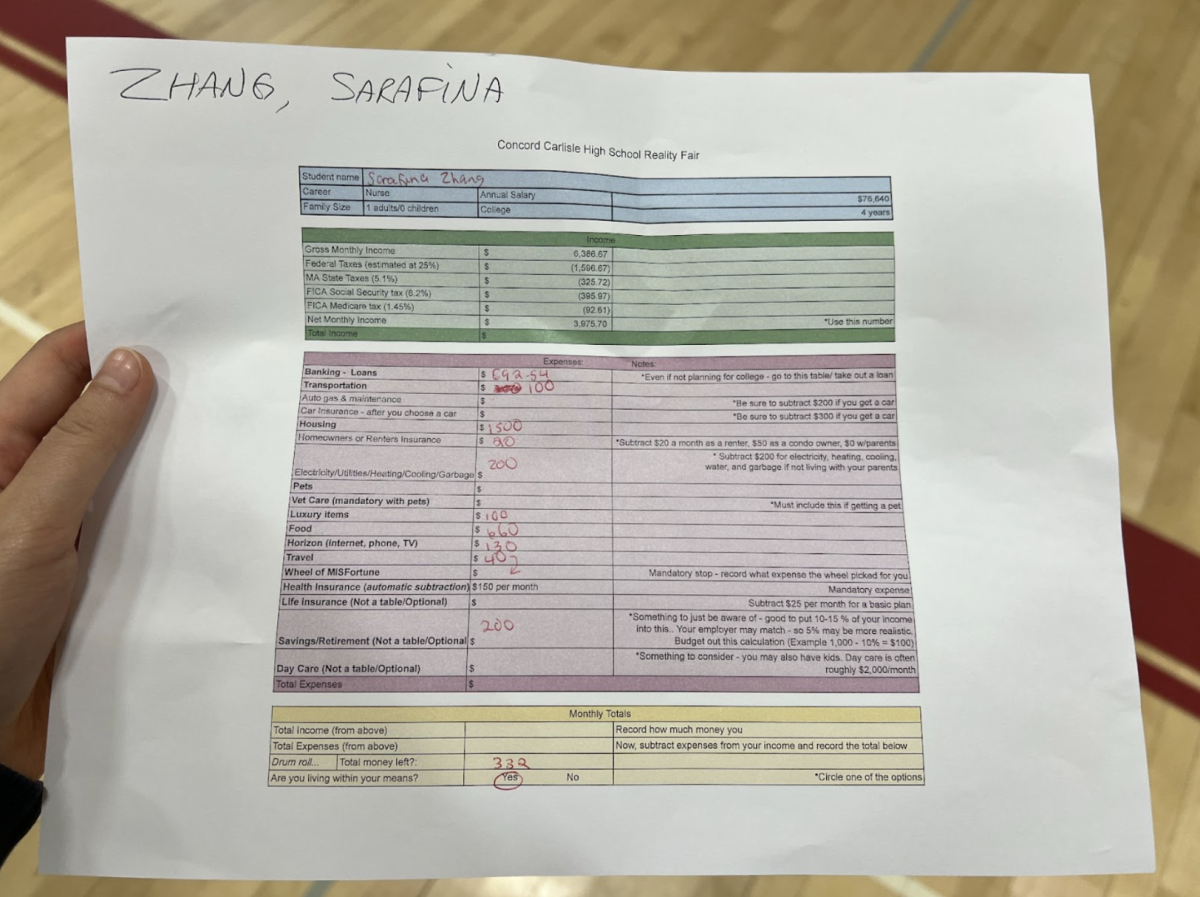

In the beginning, each student was given a detailed life biography with randomly selected economic factors such as career, family size, income, and education level. The sheet, which included the annual salary, net monthly income, expenses, and monthly totals, acted as a monthly budget template for students.

The profession I got was a nurse with an annual salary of $76,640, who lived alone and went to college for four years. My gross monthly income was $6,386.67, but after various taxes, my net monthly income came to be only $3,975.70. One student comically remarked, “Why is FICA on there twice? Wait…, what is FICA?” To be honest, I didn’t even understand all the different types of taxes that ate away over one-third of my gross income.

It may be tempting for many people, especially young adults who are new to financial situations, to live without a plan and spend money on whatever they want. However, it’s important for one to track all of their expenses to ensure they don’t fall into a vicious cycle of debt.

In the sheet, the expenses were categorized into the following: Banking – Loans, Transportation, Housing, Pets, Vet care, Luxury Items, Food, Internet/Phone/TV, Travel, and optional additions including Insurance and Retirement Savings.

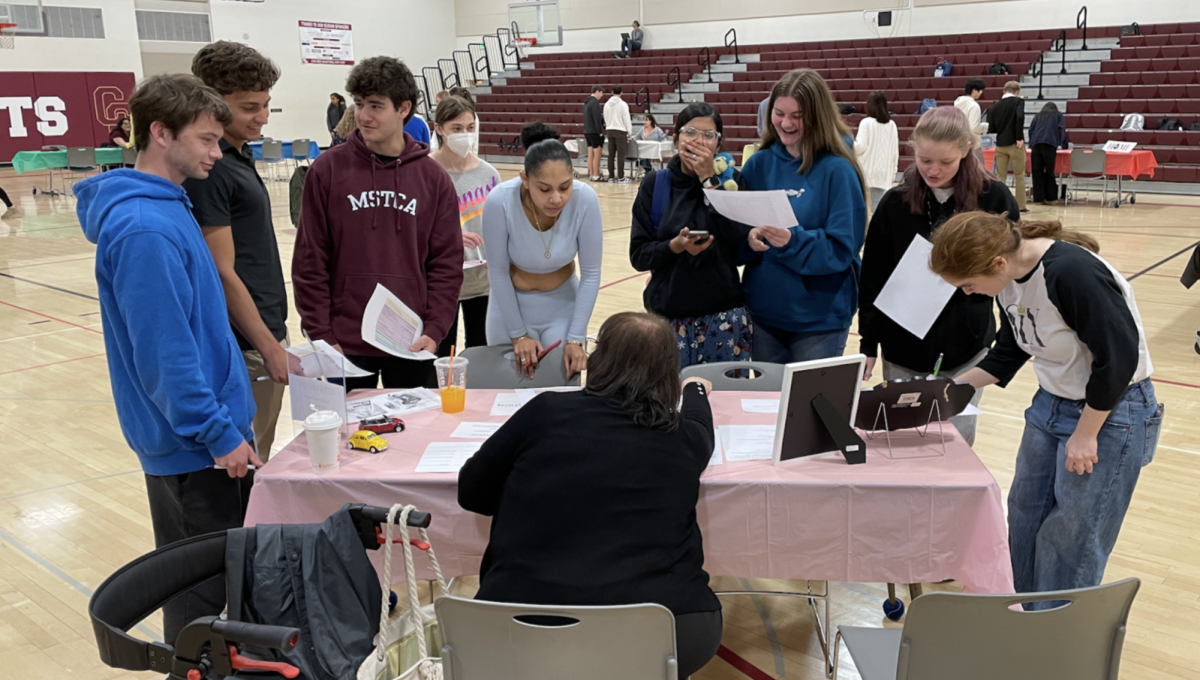

There were tables throughout the gym, one for each expense category. At each table, a community member in the business would explain the expense, present a few options of plans with different prices (per month), and guide the student into choosing the plan that is best suited for their profession and income.

The goal of this activity was to end up with less total expenses than income, and thus live within one’s means. Let’s see if I was successful in reaching this goal!

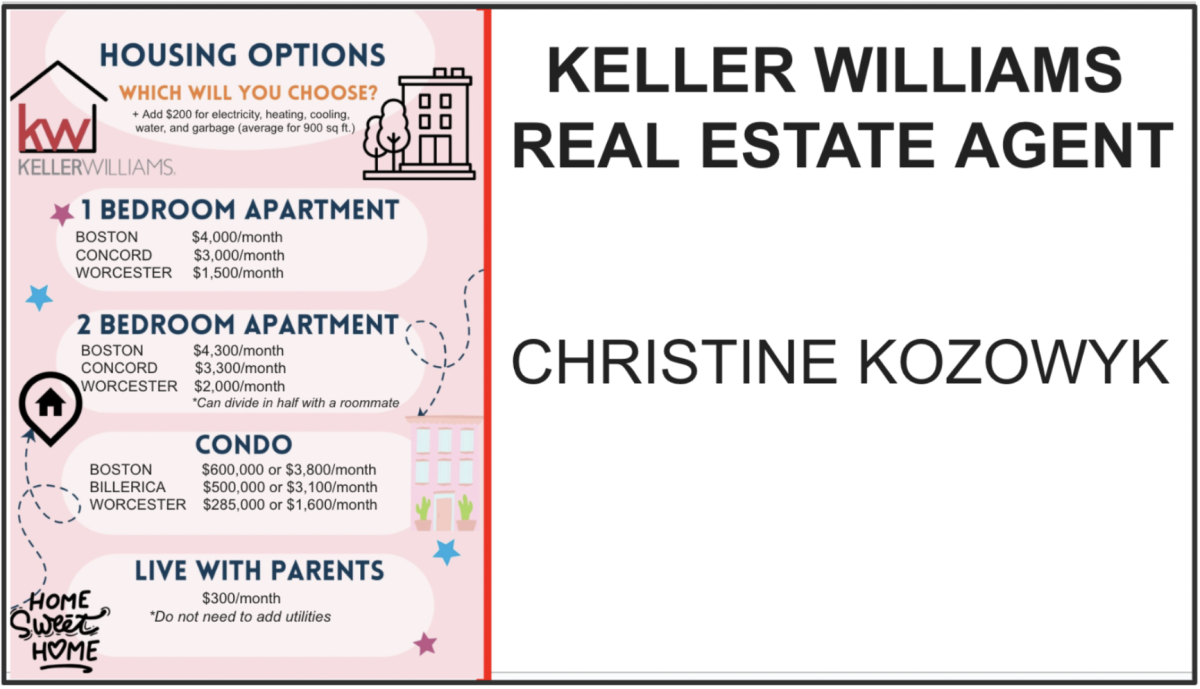

I first checked out the Housing table and spoke with a Keller Williams’ real estate agent. The options were categorized into two: home type and location. The home types were in various areas around Concord, with options for one-bedroom apartments, two-bedroom apartments, condos, or living at home with parents.

Among the home types, I found that one-bedroom apartments were more affordable than condos, but two-bedroom apartments could be the most affordable if splitting the monthly rent between two people. Condos could be bought, but it would be more costly and most likely require borrowing money by taking out a loan from the bank. I felt that for a young nurse, it would be more practical to rent for a few years before taking out a loan for a condo or house.

However, for renting, the bigger difference in cost lies in the location choice. Boston was the most expensive place to live, Concord was in the middle, and Worcester was the most affordable. One student commented, “Oh my gosh, I definitely can’t afford to live in Concord.”

The last option, living with one’s parents, would cost close to nothing in comparison to the other choices. Exasperated, another student declared, “I’m just going to live with my parents for like forever.” (Every parent’s worst fear.)

I eventually decided to rent a one-bedroom apartment in Worcester, which cost $1500 per month. Unfortunately, the rent wasn’t the only thing I had to pay when it came to housing, though; I also had to pay $20 for renter’s insurance and $200 for utilities.

Afterward, I headed to the bank table, which was directed by the Middlesex Savings Bank. As a nurse, I had attended at least four years of college already, so I had over $60,000 of student loan debt to pay back to the bank, which, split over 10 years, I learned could cost roughly $692.54 per month. At this point, after visiting only two tables, I was already budgeting for over $2,000 in expenses, and I hadn’t even visited the other seven tables yet.

Next, I went to the Luxury Items table. Examples of luxury expenses were retail/shopping, self-care, concerts, and sporting events. I decided to choose retail/shopping, which was $100 per month. This way, I knew I would have at least a hundred dollars set aside for things I might want to buy each month.

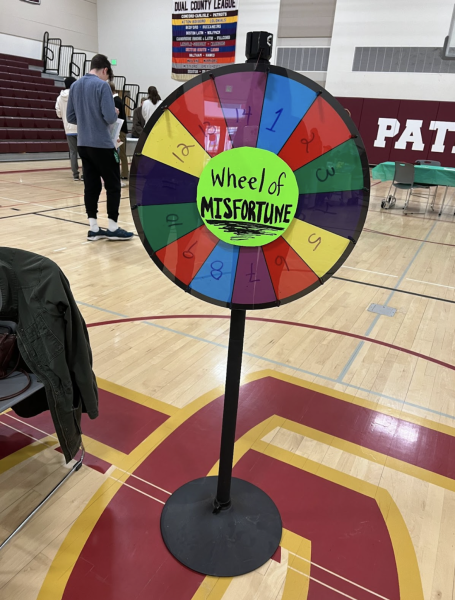

I then passed by the Wheel of MISfortune, which portrayed the mandatory expenses of unlucky setbacks and emergencies that are all too often a reality in life. A former CCHS teacher, Linda Vice-Hicey, was in charge of the wheel and told me that each number on the wheel represented a different event that would cost me money. After I spun it, the situation I got was that my friend was planning to get married and I needed to travel to attend their wedding. Hence, I went to the Travel table to see how much that would cost.

The cost of travel depended on the distance of the destination from Massachusetts. In this example, I was not sure exactly where my friend wanted to go for their wedding, so I assumed they would stay local. In total, the trip cost $480, but dividing it by 12 months resulted in the final cost of preparing to set aside $40 a month. Phew, luckily that wasn’t too bad! Others, I learned, had international wedding expenses or astronomical vet charges, that would only be less if pet insurance had already been purchased.

I knew that food would be another substantial expense, so I went to that table next, which was managed by a local business, The Concord Market. Buying groceries each week and cooking meals was the most affordable, pre-made meals were in the middle, and eating out at restaurants and ordering takeout was the most expensive.

I was surprised by how big the price difference could be between different food plans. For example, as the representatives explained to me, homemade mac and cheese would likely cost $1.68 per serving if cooked from individual ingredients, but pre-made mac and cheese could cost $7.19 per serving if bought from Concord Market; and that’s not even the restaurant price! Another example was with mangoes, where the cost of pre-packaged and cut mangos was significantly higher than a mango from the grocery store, even though both contained the same quantity of fruit.

I chose the plan with a blend of groceries and pre-made meals, which cost $660 per month. I felt that this would be a good option for a nurse because even though this plan cost more than the one with only groceries, nurses can have rough days where they would need a quick and easy meal and likely wouldn’t have the time or energy to cook from scratch.

After, I headed to Horizon, a spin off on a local business, to view their phone/internet/TV plans. I felt that phone and internet services were necessities in the modern world. TV, on the other hand, was a nice thing to have, but unessential, especially since many TV programs can be viewed online. To save money, I skipped out on TV and budgeted for $130 a month for phone and internet.

By this time, most of my expenses were written down. The only expenses left were transportation, pets/vet care, and ones from the optional categories. Since I was running out of money, I felt that it was impractical to have a pet, as I would need to pay for both the pet itself and the vet care. Consequently, for my last table, I headed to the transportation table.

I could either budget for a new car, a used car, use public transportation, or use none of these options and travel by foot or bike, which ultimately would be free, assuming I had a bike. At first, I wanted to get a used car, which would be $300 per month, but I realized that I would have to pay an additional $500 per month– roughly $200 for gas and minor maintenance, and $300 for car insurance due to my age. I also considered the fact that I chose to live in a city where public transportation would be prevalent, which meant a car wouldn’t be a necessity for me. In the end, I set aside $100 a month for public transportation.

For the optional expenses, I decided to listen to the suggestion in the “notes” box and invest 5% of my income, around $200, into a retirement savings account. I did this because I was informed that employers would usually match up to 5% of a retirement savings contribution–which is basically free money–and I believed that starting to save for retirement early would be beneficial for my future.

Now, it’s time to see how well I did with my budgeting. Did I spend less than I made this month? Or, did I end up with more debt? I added up all my expenses, which came out to be around $3,443. Then, I subtracted this number from my net monthly income, $3,975.70, to get $332 as my total amount of money left. I succeeded! I was extremely happy to see that I was able to budget wisely and live within my means, while still having all the essentials and even some leeway for luxury items and my future retirement. However, I must say, this required a considerable amount of effort. I related a bit too much with another student when one of the seniors said, “I don’t want to be an adult.”

Budgeting is one skill under the umbrella term of financial literacy. You may be wondering, what is financial literacy? Investopedia defines it as “the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing.” You wouldn’t be the only one to ask this question. According to a study from Marketwatch, “Only 57% of adults in the United States are financially literate.” Alarmingly, this rate is even lower for Gen Z, the generation of current high school students. Zippia finds, “Only 36% of Gen Z are financially literate.” One of the reasons for this is that many schools do not teach financial literacy, and parents who aren’t financially literate don’t have the ability to educate their children about it.

The lack of financial literacy has led to a nationwide crisis. Over the past 50 years, the American middle class has been shrinking due to inflation–the rise in prices of goods and services–and the wealth gap is increasing. Zippia continues, “63% of Americans live paycheck to paycheck. Approximately 125 million Americans live paycheck to paycheck week after week.” This has led numerous people to ask the question: Why are our schools not teaching students how to become financially literate?

States have stepped up to address this problem. According to NBC News, “Twenty-five states currently require financial literacy for high school students to graduate.” However, Massachusetts is not one of them. The reality fair aims to give CCHS’ graduating seniors a low-stakes and fun glimpse into the reality of financial situations so they won’t be as startled when they soon encounter these in real life.

At the fair, students also got the opportunity to connect with experienced community members in various professions–from realtors to bankers–at each table to receive personalized advice. Kai Macy explained, “When I was doing the budgeting fair I wasn’t only trying to save money, but I was trying to find ways to make money. I’ve heard about Section 8 and how it is a pretty safe investment as one receives payment from the government. I also have done a little research on FHA loans and how you can get a really low down payment as a first-time home buyer. These two things not only helped me save money on monthly expenses but will make me money in the future.” Another senior, Hannah Daniel, admits that “it was a good reality check for us as we enter the real world.” She adds that it “would be great for more people to see and experience the reality fair before leaving high school.”

I really enjoyed the reality fair, because it was both fun and informative. Many students feel overwhelmed by the thought of learning about managing one’s finances at first, because it may seem super complicated and adult-y. However, the fair’s game format knocked down this barrier by allowing them to go through a real-world example of budgeting in an entertaining way with their peers. Overall, the reality fair was an amazing initiative and illustrates CCHS’ commitment to giving seniors a head start on their journeys to financial literacy.